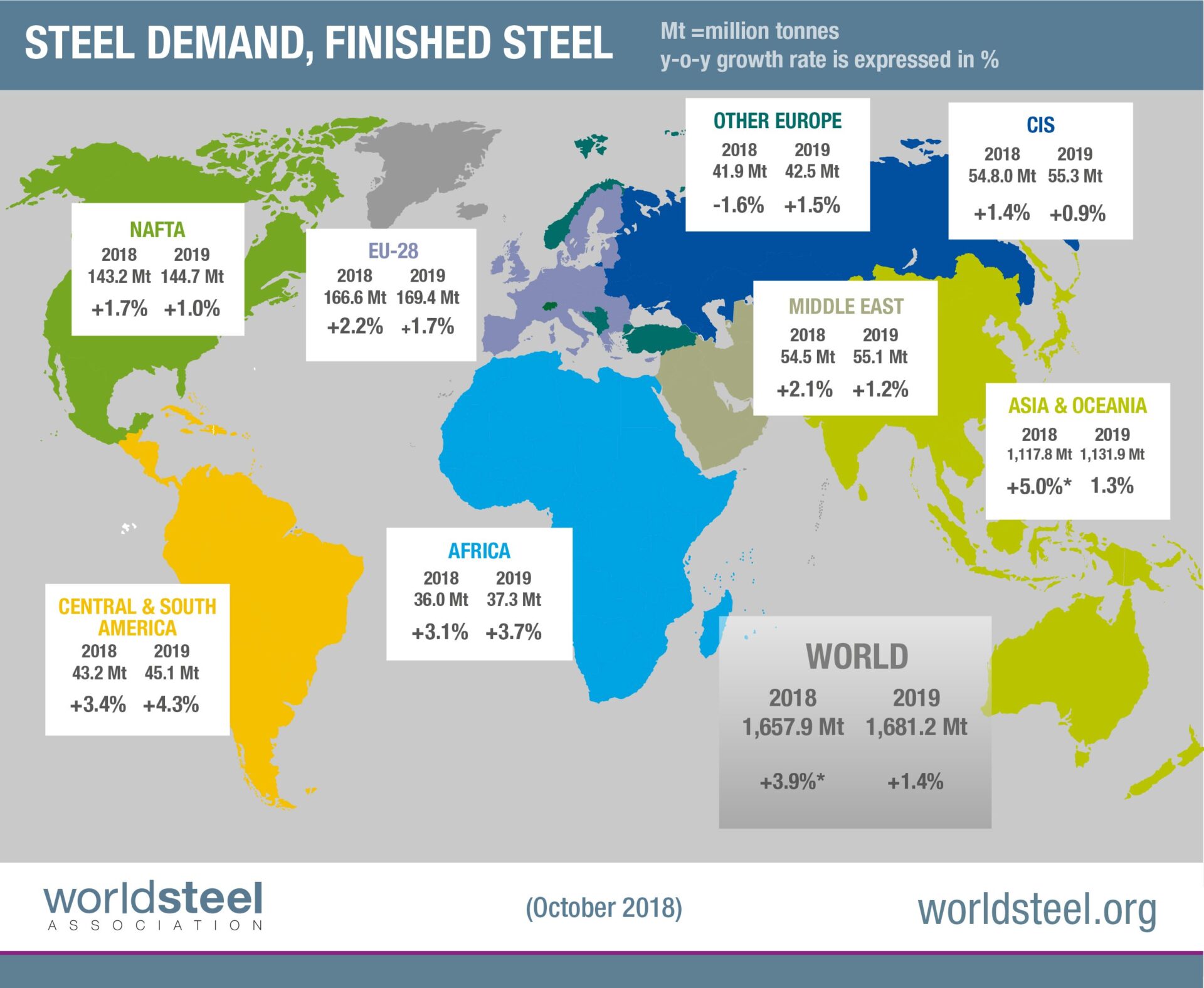

Commenting on the outlook, Mr Al Remeithi, Chairman of the Worldsteel Economics Committee said, “In 2018, global steel demand continued to show resilience supported by the recovery in investment activities in developed economies and the improved performance of emerging economies. Demand for steel is expected to remain positive into 2019, growing at 1.4% globally.”

Global steel demand faces uncertainty from tensions in the global economic environment

While the strength of steel demand recovery seen in 2017 was carried over to 2018, risks have increased. Rising trade tensions and volatile currency movements are increasing uncertainty. Normalisation of monetary policies in the US and EU could also influence the currencies of emerging economies.

China steel demand growth is expected to decelerate in the absence of stimulus measures

In the first half of 2018, Chinese steel demand got a boost from the mini stimulus in real estate and the strong global economy. However, continued economic rebalancing efforts and toughening environmental regulations will lead to deceleration of steel demand toward the end of 2018 and 2019.

Both downside and upside risks exist for China. Downside risks come from the ongoing trade friction with the US and a decelerating global economy. However, if the Chinese government decides to use stimulus measures to contain the potential slowdown of the Chinese economy in the face of a deteriorating economic environment, steel demand in 2019 will be boosted.

Steel demand in the developed world remains healthy, but growth will moderate

Steel demand in developed economies is expected to increase by 1.0% in 2018 and 1.2% in 2019. US steel demand grew strongly in 2017, benefiting from strong consumer spending and business investment supported by tax and regulatory changes and fiscal stimulus, although growth in the construction sector moderated. Steel demand growth in 2019 is expected to slow as auto manufacturing and construction activity is expected to see modest growth. The manufacturing sector is expected to perform well thanks to the strength of the machinery and equipment sector.

The broadening recovery of EU steel demand is expected to continue, though at a reduced pace, mainly driven by domestic demand. With business confidence high, investment and construction continued to recover while the automotive market may see slower demand growth. Though the economic fundamentals of the EU economy remain relatively healthy, steel demand in 2019 will show some deceleration over the growth seen in 2017-18, partly due to uncertainties resulting from global trade tensions.

Steel demand in Japan is expected to remain stable due to supportive factors on investment (record-high corporate earnings, the continuation of monetary easing, demand associated with the Tokyo Olympics and the increasing need for labour-saving investments). Steel demand in Korea will contract further in 2018 with all its major steel using sectors struggling. Only a minor recovery is expected in 2019.

The developing world’s steel demand recovery continues, but is facing challenges

As India recovers from the twin shocks of demonetisation and the goods and services tax (GST) implementation, India’s steel demand is expected to move back to a higher growth track. Steel demand will be supported by improving investment and infrastructure programs. Stressed government finances and corporate debt weighs on the outlook.

Sluggish construction activities and stock adjustments led to slow growth of steel demand in the ASEAN region in 2017 and 2018, but demand in the ASEAN region is expected to resume its growth momentum backed by infrastructure programmes in 2019 and onwards. Risks are largely related to rising trade tensions between the US and China, currency volatilities and political instability. Steel demand in developing Asia excluding China is expected to increase by 5.9% and 6.8% in 2018 and 2019 respectively.

In the remainder of the emerging and developing economies, the recovery has been slow to gain momentum, with rising uncertainty in both domestic and external environments. Structural reforms, high financial market vulnerability and possible currency pressures from the tensions in the global economy are amongst the main reasons.

In the Gulf Cooperation Council (GCC) countries, reforms and a stronger oil market have led to an upward momentum in steel demand, but at a slow pace. The outlook for Iran has turned less favourable due to the reinstatement of sanctions by the US.

Even with the rise in oil prices, growth in steel demand in Russia is expected to show weak momentum.

Turkish steel demand is expected to contract in 2018 with the currency crisis it has faced, but the government’s stabilisation measures and a consequent return to the competitiveness of the manufacturing sector is expected to help recovery in 2019.

Steel demand in the Latin American economies is continuing its second year of recovery backed by positive developments in the domestic and the global economy. Steel demand in Brazil continued its stable recovery in 2018. This will continue into 2019 as election fever subsides. Steel demand in Mexico has suffered from uncertainties related to the NAFTA negotiation and the election, but the recent signing of USMCA and the new President calming jittery markets are expected to help the economy to recover slowly in 2019. Steel demand in the emerging economies excluding China is expected to grow 3.2% and 3.9% in 2018 and 2019 respectively.

Mixed outlook for the construction sector and automotive market in many countries

In the developed economies, growth in the construction sector is likely to moderate after the strong recovery momentum seen in 2017-18 due to a high base and rising interest rates. On the other hand, construction activities in most developing economies will continue to grow, notably in India, ASEAN and MENA. However, Brazil’s construction sector has not yet started to recover from its deep crisis.

The automotive markets which showed strong growth in the developed economies are softening on the back of slowing demand growth, rising fuel prices and interest rates. In the developing countries, demand for automobiles will continue to grow at a healthy pace. The machinery sector in both the EU and US continues to be supported by a strong business investment phase.